Effective pricing methods that maximise profit

With data-driven and value-based pricing solutions, you'll learn how to listen to your customers, bring informed decisions and reach your revenue/profit targets. Drive long-term growth and get a competitive advantage guided by our expertise and deep industry knowledge.

Commonly solved business questions

Are our prices aligned to the customer value?

By measuring brand equity, evaluating price perception, and using sell-out prices, boobook identifies how well current pricing is aligned with the perceived brand value. Following this, we also measure price elasticity to advise the right price strategy.

How resistant are our brands to price increases?

Willingness to pay, or price elasticity, is valuable information every brand should know and understand. We support companies in measuring price elasticity by analysing existing transactional or market research data. The analysis results in a demand curve used as input to any ‘what-if’ scenario, such as future price increases.

Who are our biggest competitors in terms of brand power?

Any company/brand operates in a competitive environment. Through consumer listening and analytics, we provide insights into how a brand compares to its key competitors regarding brand performance, image, and price elasticity.

How do I build pricing expertise capabilities in my team?

While at boobook, we often build pricing strategies for our clients based on consumer understanding, we also support some of our clients on how they can develop value-based pricing expertise in-house. We take our clients through various training and coaching sessions, from business goal definition to translating insights into a strong pricing plan.

Is my brand more or less price elastic versus competitors or versus the sector?

Over the past 20 years, boobook has conducted pricing research across many industry sectors and brands, including measuring price elasticity. Hence, we built a massive database with benchmarks, as any number is only useful when it can be compared to something else.

Should we go for monthly licence fee pricing or stick to one-off payment?

The “Netflix model” is gaining popularity among many companies and products as it offers a long-term revenue stream, including upsell strategies. But how do consumers react, and what is their willingness to pay when moving to a monthly subscription? Through various consumer understanding techniques, such as conjoint, we measure consumers’ appetite for different pricing models. We translate the insights into sustainable and profitable pricing strategies.

Insider insights on pricing

Level up your business with inspiring articles where we share our knowledge and practical know-how.

The AI-feature trap: is your brand worth its price tag?

Artificial intelligence is not just changing how people shop. It is changing the rules under which brands compete.

As AI tools make price comparison and feature benchmarking effortless, competitive landscapes become structurally more transparent. Specifications are extracted, ranked and displayed in seconds. Prices are surfaced without friction, increasing price awareness among consumers.

This is not a technological evolution. It is a strategic shift. If your offer can be reduced to structured, measurable attributes, it will be. And when measurable attributes dominate the comparison, price quickly becomes the most visible point of differentiation. In this environment, brands will need to prove more than ever that they are worth their price tag.

The feature trap: when functional dominates, price follows

AI systems are designed to structure information. They parse product pages, extract specifications and rank comparable attributes. In doing so, they privilege what can be measured: performance scores, technical features, material composition, size, speed, capacity.

When products or services are reduced to structured specifications, the purchase decision risks collapsing into a trade-off between measurable features and price. The richer layers of brand meaning become less visible in the comparison interface.

This is what we call the feature trap: when the architecture of comparison makes price the most salient lever.

Brand equity as a strategic shield

Strong brands show that pricing power does not stem from functionality alone. Customers routinely choose more expensive options despite credible and cheaper alternatives. Not because they failed to compare, but because they value more than the spec sheet reveals.

Patagonia is a clear example. In a category where many brands offer technically comparable outdoor apparel, customers willingly pay a premium. The differentiation does not live solely in fabric weight or water resistance. It lives in purpose, identity, credibility and the total experience of engaging with the brand.

The same dynamic can be seen in brands such as Ben & Jerry’s, Apple, Starbucks and Rituals. Their products can easily be compared on functional attributes, yet customers are willing to pay more because the value extends beyond the product itself.

Besides functionality, there are three other dimensions that determine value:

- Emotional: the feelings, identity and meaning a brand evokes

- Trust: the credibility and reliability consumers associate with a brand

- Experience: the total customer journey before, during and after purchase

AI comparison tools heavily favour the functional dimension. They are far less capable of capturing emotional resonance, accumulated trust or the lived experience of being a customer.

For brands with shallow equity, this asymmetry is dangerous. Their competitive advantage resides mainly in functional claims, which are easy to benchmark and easy to imitate.

For brands with deep equity, AI becomes less of a threat. Their value proposition extends beyond what can be neatly organised into comparable data points. Customers’ willingness to pay is anchored in something broader than specifications.

Pricing power is about willingness to pay

Pricing power emerges when customers perceive sufficient value to accept a higher price and remain relatively insensitive to changes within a certain range. Strong value perception raises the ceiling of willingness to pay and reduces price resistance. It also creates differentiation across segments: some customers are willing to pay significantly more because they value specific dimensions more strongly.

To avoid competing purely on price, brands must understand which elements of value truly drive willingness to pay, and how these differ across customer segments.

Customer insight as the engine of pricing power

To gain these insights and rebuild pricing power, you need to listen to your customers. Understanding the role of functional, emotional, trust and experience value starts with measuring how important each of these dimensions is for your brand.

The next step is to identify the drivers behind each dimension: which specific elements shape functional value, build trust, create emotional connection or strengthen the customer experience. These drivers may differ across customer segments, as different groups of customers value different aspects of an offer and are willing to pay different prices for them.

A combination of qualitative and quantitative research, complemented by market data and web scraping, helps build a clear understanding of what value means for your brand. Next you can quantify how that value translates into pricing power by measuring willingness to pay and price elasticity.

There are different approaches to measuring this, ranging from simple survey-based methods to more advanced techniques such as conjoint analysis, historical sales analysis or price experiments. Each method comes with its own trade-off between complexity and accuracy.

Competing on value in an AI-driven market

AI will continue to increase transparency. It will continue to make feature comparison faster and price differences more visible. That trajectory is unlikely to reverse.

The strategic response is not to resist transparency. It is to ensure that what becomes transparent includes more than just specifications.

Brands that invest in building and measuring multidimensional value can withstand comparability because their differentiation lives beyond the spreadsheet. Their pricing power is anchored in perception, trust and experience, not just in technical performance.

The real question is: is your brand equity strong enough to ensure that, even in a perfectly comparable environment, customers will still choose you? In other words: are you worth your price tag?

Need help mapping the drivers of your value and identifying how you can increase willingness to pay? Let’s talk.

Unlock price potential: how to master value-based pricing

Rising material and labour costs, decreasing purchasing power, a competitive market and high promotional pressure: no wonder many companies struggle with price setting in today's economy. There is unfortunately no ready-made formula to follow. Understanding your brand, product, market and customers is essential to get your pricing right. Building a pricing strategy without these insights is like building a house on quicksand. An insight-driven method such as value-based pricing is not the easiest to implement, but it is rewarding in the long run. It allows you to maximise your price potential, especially if combined with increased brand equity as this will result in lower price elasticity.

The importance of a strategic approach

How loyal are your customers? Do you understand how competitors set their prices? What is the price elasticity of your brand compared to competitors? How resistant are they to inflation? Do you know what your customers value the most: your brand, product quality or package design?

If you rely solely on gut feelings to answer these questions your current pricing strategy might be suboptimal. Whether you choose cost-plus, competitive-based or value-based pricing, you always need a certain amount of data and insights to set the right price. Unlike the other methods, value-based pricing requires a deep understanding of your customers and consumers in general, viewing price as an expression of the value you offer. It is the only approach that allows you to maximise your price potential while building brand equity, because once you know what consumers and customers value and what drives their choice, you can deliver an offer tailored to their needs. This often results in a higher willingness to pay.

5 steps to value-based-pricing

Working with our clients, we have seen time and time again that there are five important steps to implement this approach successfully. The overall company strategy should always be your starting point (1), ensure the price is in line with the brand, product and consumer (2), listen closely to consumers and customers (3), create a win-win for all channel partners (4) and analyse whether your market research data is in line with pre-existing knowledge (5).

- Start from the overall company goal

Although it might seem obvious, it is not always clear why a company wants to adjust their prices. Do you want to focus on volume, revenue, profit or even increasing customer satisfaction? If your goal is increasing volume, you will probably lower your prices, whereas optimising profit might mean higher prices. The KPI you decide to focus on determines your optimal price, as optimising all is rarely possible.

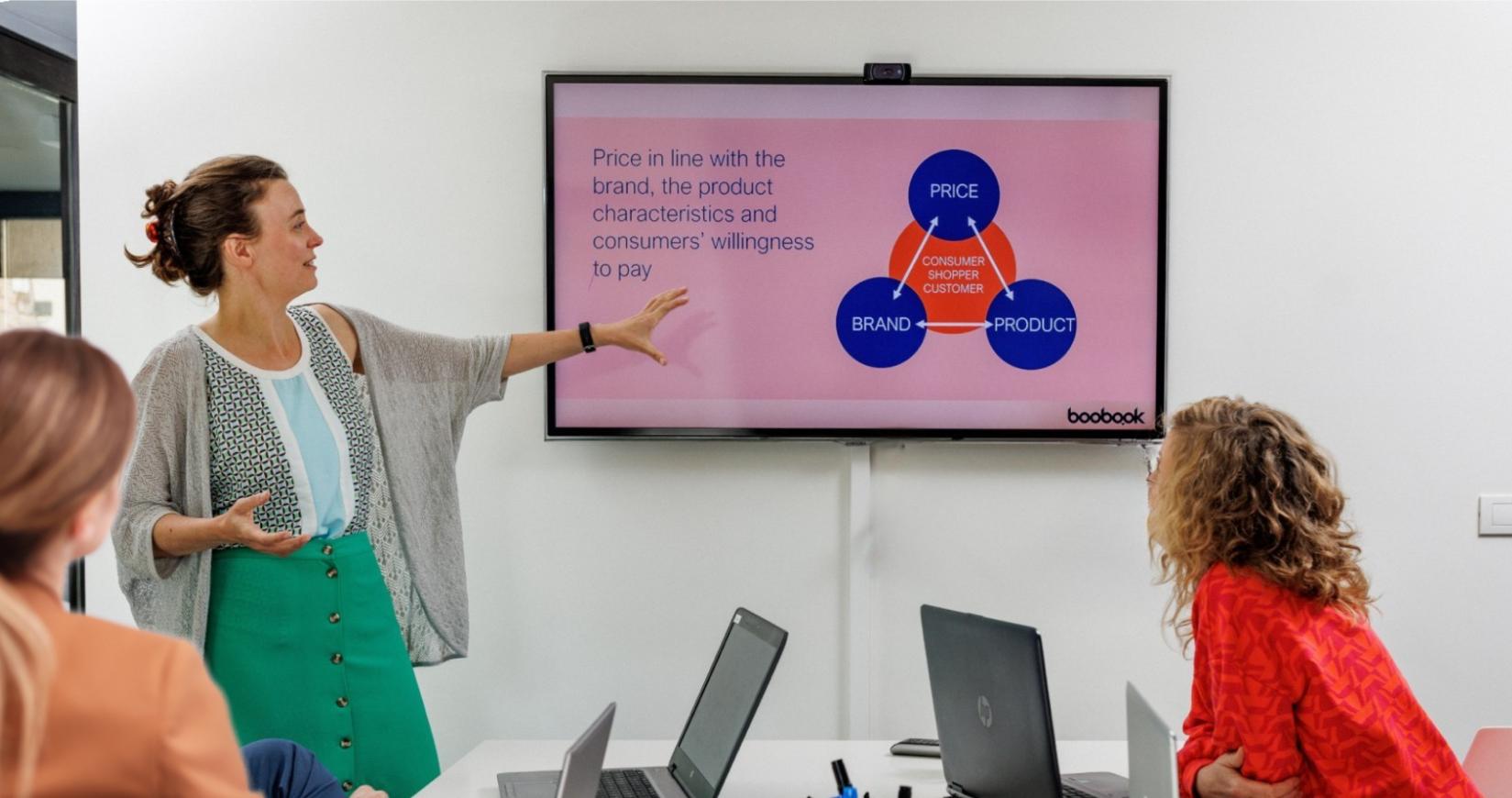

- Look beyond price and business KPIs

Regardless of the KPI you prioritise, price isn’t a standalone feature. It should always be aligned with your brand, product or service and target consumer or customer.

- Whether consumers think of your brand as trusted, premium or trendy will impact the price they are willing to pay.

- Do you understand why people choose your product? Is it the brand or packaging design? The colour or product quality? This influences the price you can ask.

- And what about your consumers and customers? How price sensitive are they, and are they all equally sensitive or are some segments willing to pay more because they truly love your products or brands?

- Listen to the customer

You will need data to identify the customers’ willingness to pay and your brand’s price elasticity. It will also allow you to understand how customers value your products. A combination of methods will help you achieve this. Transactional data capturing customers’ past behaviour enables you to predict the impact of past price changes on sales. Qualitative research gives more insights into the value drivers and willingness to pay, especially for customers who are hard to reach. Various quantitative methods (such as Van Westendorp, Gabor Granger or conjoint analysis) will help you predict future behaviour for pricing scenarios that have not yet been seen in the market.

- Create a win-win for all channel partners

No matter how solid your price strategy is, it will fail if you don’t get your partners to agree and adapt their prices accordingly. Share your knowledge with them, educate them on consumer insights and possibly split some gains to get them on board and build long-term relationships.

- Build your final price setting on four inputs

Lastly, avoid solely relying on market research for your new pricing strategy. Make sure it is aligned with the company strategy and take internal knowledge, expertise and existing data into the equation. Talk to as many stakeholders as possible and capture their insights, especially if your business has been around for quite some time and already navigated many challenges. Build on the experience you already have.

Keen to know more about value-based pricing and how to optimise your price potential? Get in touch!

Pricing strategy isn’t one size fits all

Our approach starts by understanding your business challenge thoroughly, asking the right questions, and crafting a customised strategy by blending different methodologies.

Conjoint analysis

Conjoint is an elite pricing tool that gauges consumer preferences and product elasticity. Its simulator identifies optimal pricing for maximum profit.

Transactional data analysis

Prioritizing customer feedback over transactional data aids in accurate predictions. Analyzing data correlations using machine learning refines market strategies, but past data has its limitations.

Gabor Granger

This pricing method presents customers with varying price points for a product and asks their willingness to purchase, resulting in a demand curve that identifies optimal pricing for maximizing sales, revenue, and profit.

Insights that empower businesses, regardless of the sector

For over 20 years, we’ve been working closely with international clients from various sectors, supporting them in achieving outstanding results. Our approach is based on personalised solutions that tackle the specific challenges of each industry.

Retail and FMCG

In a highly competitive retail and consumer market, brands need to adapt to inflation and address consumer concerns about eco-friendliness, sustainability, and health. We offer guidance on staying competitive through product portfolio optimisation, value-based pricing strategies, and streamlining offerings.

Technology and software

The technology industry is constantly evolving, shifting towards subscriptions, cloud-based solutions, multi-platform compatibility, and AI-driven innovations. We provide expert guidance on product development, refining pricing models, and positioning brands for growth and market leadership.

Hospitality and entertainment

The entertainment and hospitality sectors face unique challenges as the pursuit of pleasure and sustainability often seems at odds. Additionally, in today's world, are consumers still willing to spend money on unique experiences and luxurious holidays? We advise companies on refining holiday products, including implementing the right pricing strategy, to meet current consumer needs.

Luxury industry

Value-based pricing is the cornerstone of the luxury industry. While the target audience for luxury products often has more disposable income, they are also more discerning and have specific needs. We translate these needs into clear pricing strategies that enhance profitability and drive sustainable growth for luxury companies.

Manufacturing

When your customer is not the end consumer and multiple players are involved in the sales chain (resellers, wholesalers, retailers), it can be tricky to optimise product development and set prices. We provide advice on creating an optimal product, pricing, and promotional strategy that benefits you, your customer, and the end consumer.

The 3-step framework made for success

Alignment and input workshops

In the initial phase, we work closely with you to understand your business needs, objectives, and knowledge gaps. Through interactive workshops, we align on the project scope, discuss the business context, and gather enough input so we can help you define your goals and create the winning strategy.

Consumer/customer listing

In the second stage, we carefully listen to your customers/consumers and delve into existing data, leading to invaluable insights about both your products and of your competitors. This customer-centric approach guarantees well-informed strategies driven by the needs and preferences of your target audience.

Learn, act and optimize

In the final phase, we turn data and knowledge into action plans. Thanks to business expertise, in-depth analytics, and effective storytelling, we provide wisdom through practical recommendations. We help you implement, monitor, and optimise your customer-oriented strategies for sustainable growth.

Unlock the secrets to success

Take examples from successful companies who collaborated with us and found the right answers to important business questions.

.png)

.png)

.png)

Set your business up for success

Realise your business's efficiency and achieve success by optimising and harmonising the four pillars of excellence: price, brand, product, and customer. Building a thoughtful strategy for each - and aligning them - will refine your overall marketing strategy, enhance your customer journey, and boost profitability.

.jpg)

Make better

business decisions

Explore our success stories and learn how we've successfully helped different businesses. Or get in touch with us to schedule an introductory call.